Any property investor can agree that taxes are the bane of their existence and definitely not the object of all their desires but are of course necessary!

If you purchase a property through a limited (LTD) company or SPV (Special Purpose Vehicle), it can result in several potential tax benefits and increased asset protection.

However, before you start investing, it’s essential to understand the intricacies of buy to let mortgages for limited companies.

As mortgage advisors we will focus on the mortgage related side within this piece and will always advice you speak to a qualified tax adviser in this area initially.

Hence, in this informative article, we’ll take a detailed look at buy to let mortgages for limited companies, its pros and cons for property investment and much more.

Table of Contents

- What Is Buy To Let Mortgages For Limited Companies?

- What Is A SPV Or Special Purpose Vehicle?

- What Are The Benefits Of Buy-To-Let Mortgages For Limited Companies?

- What Are The Drawbacks Of Buy To Let Mortgages For Limited Companies?

- Eligibility Criteria For Getting A Limited Company Buy-To-Let Mortgage

- How To Get A Buy-To-Let Mortgage Through A Limited Company?

- How To Set Up A Property Company For Buy-To-Let Purchases?

- Conclusion

What Is Buy To Let Mortgages For Limited Companies?

A buy-to-let mortgage for a limited company is a type of mortgage used by a company to purchase a property for the purpose of renting it out.

Unlike traditional buy-to-let mortgages, which are taken out by individuals, these mortgages are specially designed and owned by the limited company.

With buy to let mortgages for limited companies, the company is the borrower, not the individual actually borrowing.

As a result, the mortgage is based on the financial status of the company.

Interestingly, after April 2017, a lot of landlords began opting for limited-company BTL mortgages over personal ones, owing to the amendments made by the UK government in the 2017 Budget.

The aforementioned stated a significant decrease in the amount of tax relief provided for interest on BTL mortgages.

What Is A SPV Or Special Purpose Vehicle?

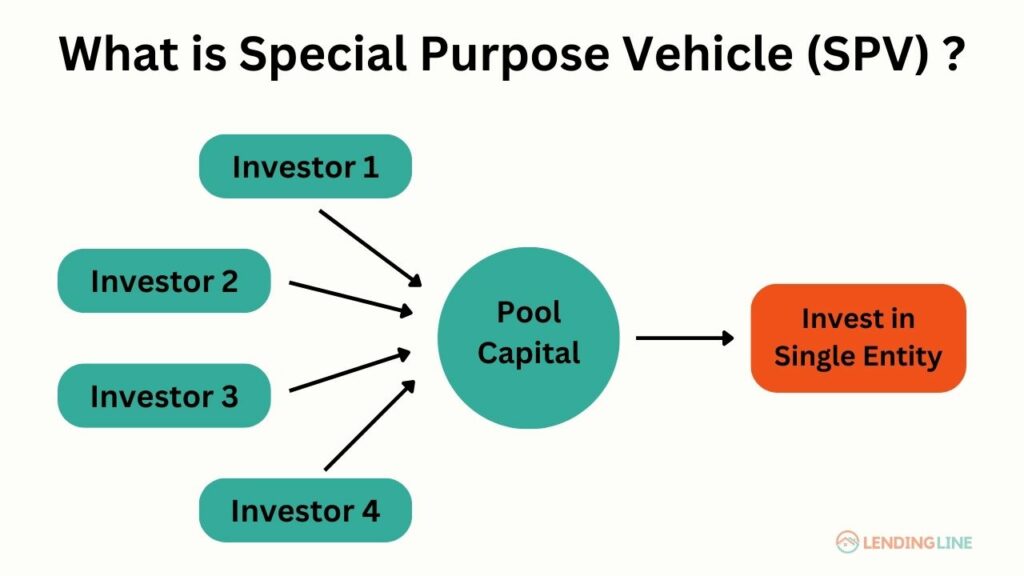

As we mentioned earlier, taking out a buy-to-let mortgage can be more tax-efficient when done through a company or special purpose vehicle (SPV) in certain circumstances. But what does a special purpose vehicle mean?

The definition on Investopedia says, “ A special purpose vehicle, also called a special purpose entity (SPE), is a subsidiary created by a parent company to isolate financial risk. Its legal status as a separate company makes its obligations secure even if the parent company goes bankrupt. ”

Basically, it is a legal entity that is created for a specific, “limited” purpose. It is typically set up as a subsidiary company or a separate entity altogether and can be used for a variety of purposes, in this case property investment.

In the context of property investment, an SPV is usually a vehicle used for purchasing and holding buy-to-let properties. By setting up an SPV, investors can create a separate legal entity that is distinct from their personal finances.

However in all instances personal guarantees will need to be given by directors with very similar rules also for shareholders who are not directors.

The profits made by an SPV are subject to corporation tax and others taxes, which could be more beneficial than income tax rates based on the circumstances of the investor where they to operate in there personal name, SPVs could be used by landlords to avail themselves of tax benefits.

What Are The Benefits Of Buy-To-Let Mortgages For Limited Companies?

1. More variety available

Since this has become a more popular route of purchasing property for buy to let investors, there is a wider variety of LTD company buy to let lenders with lending criteria and mortgage products to meet different borrowers needs.

2. Expansion Of Your Portfolio

It allows you to keep profits within the company, this approach may allow you to utilise a greater portion of your earnings to expand your property portfolio rapidly.

3. Future Planning

Transferring ownership of a limited company may be easier than that of a privately owned property.

In the case of the company, the property remains under the possession of the “company,” but its ownership changes “hands.” This may allow certain options.to suit the buy to let investor in the future.

What Are The Drawbacks Of Buy To Let Mortgages For Limited Companies?

1. Higher Mortgage Rates

The first and foremost disadvantage of buying a buy-to-let property through a limited company is in most cases the higher interest rates and fees charged by lenders.

2. Added Cost Of Running A Company

When establishing a limited company, it is important to consider the additional expenses and responsibilities that come with it. These may include:

- Legal fees

- Corporation Tax

- Annual auditing – if applicable

- Filing at Companies House

- The preparation of accounts – this is a legal requirement

- Accountants may also charge a higher fee when preparing accounts for Companies House

3. No Capital Gains Tax Allowance

A limited company does not receive a Capital Gains Tax (CGT) allowance on selling a property. Contrasting this, an individual who sells a buy-to-let property is granted a certain allowance that exempts them from paying CGT on a portion of their profits.

When it comes to buy-to-let properties owned by limited companies, you will be liable for Corporation Tax from the company (since you won’t pay any CGT). As a result, you are not eligible for the CGT allowance.

Whether this approach is financially beneficial for you will depend on the profit earned from the sale of your BTL property.

4. Fewer Options

Limited companies may not be eligible for buy-to-let mortgages from all lenders. Alongside, if some do offer such mortgages, they typically have a smaller product range.

5. Additional Conveyancing

It is important also to bear in mind the additional work involved with your conveyancing solicitor when purchasing a property through a LTD company when compared to a purchase in individual names.

Alongside more documentation there is usually a reduced panel of solicitors accepted by the lender and due to this in most cases they charge higher conveyancing fees.

Eligibility Criteria For Getting A Limited Company Buy-To-Let Mortgage

The different types of limited companies that may be considered for a mortgage include:

● A newly formed limited company at the time of purchase

● An already established special purpose vehicle (SPV) limited company The eligibility criteria will vary.

The loan-to-value (LTV) ratio can be up to 85% although primarily lower. The rental income should cover at least 125% of the mortgage payment, this is mainly the affordability calculation used for LTD companies. Moreover, a limited company with minor adverse credit can also be eligible for a BTL mortgage with certain lenders.

How To Get A Buy-To-Let Mortgage Through A Limited Company?

1. Get In Touch With A Mortgage Broker

To apply for a buy-to-let mortgage for a limited company, one can use the services of a specialised mortgage broker. They have a thorough understanding of the eligibility criteria required for mortgages.

Not to forget, many lenders of buy to let mortgages for LTD companies only accept applications through such intermediaries.

2. Contact An Accountant Or Tax Adviser

To ensure that the limited company for buy-to-let purchases is set up correctly and is right for your circumstances, you should always seek the advice of an accountant or a tax adviser.

Further, it may be beneficial to contact them before reaching out to a mortgage adviser so that element of the limited company transaction is organized and ready for the mortgage application process.

How To Set Up A Property Company For Buy-To-Let Purchases?

Creating a limited company is quite a straightforward process that can be done online or by post via Companies House. Here’s what you’ll need for the registration process:

1. Company Name And Address

When registering your company, you must provide a unique name and address.

Next, you must appoint at least one director. Of course, you can add more directors or even a company secretary.

Also, note that each shareholder should be given a percentage of the company. But any shareholder with more than 25% of the company’s shares is considered a Person with Significant Control (PSC). As such, their details will be publicly listed.

3. Definition Of Business Activity

You may have to define the company’s activities using Standard Industry Classifications (SICs) depending on the lender’s requirements.

Contact a qualified accountant when deciding the type of company to create. A tax adviser can also advise on whether it should be an SPV.

After the company is registered, it’s imperative to register for Corporation Tax within three months and in most cases set up a business bank account.

Conclusion

So, you see, buy-to-let mortgages for limited companies can be tax-efficient alternatives to traditional mortgages in personal names.

That said, the eligibility criteria will vary depending on the lender’s requirements.

Hence, seeking advice from tax advisors, accountants, and mortgage brokers is the best way to ensure that the limited company is set up correctly and ultimately is the right route for you.

**A buy to let mortgage will be secured against your property.

Some types of buy to let mortgages are not regulated by the Financial Conduct Authority.

All content is written by qualified mortgage advisors to provide current, reliable and accurate mortgage information. The information on this website is not specific for each individual reader and therefore does not constitute financial advice.

I am CeMAP & CERER qualified mortgage adviser and have helped a number of clients realise their dreams when they thought it would not be possible. I’m skilled at getting mortgages sorted for people with a history of missed payments, CCJs, defaults, debt management programmes, IVAs and bankruptcies.

I am CeMAP (Certificate in Mortgage Advice and Practice) qualified mortgage adviser with a strong background in Finance. I specialise in providing expert advice on a range of mortgage products, including first-time buyers, remortgages, buy-to-let mortgages and bad credit mortgages.